- Crypto Is Easy

- Posts

- Your Impression is Not Reality

Your Impression is Not Reality

I have met the retail investors, and they are us. July monthly issue.

In last month’s issue, I looked at where the money’s coming from, where it’s going, and why political parties won’t get you what you want (and may make everything worse).

In this month’s issue, I share some facts that may make you question the stories you’ve been told.

If you want to hear an auto-narration instead of my voice, head over to the Medium version of this post.

Crypto is a way to secure all the rights and privileges of orderly society without coercion or restraint.

At least, it will be, as soon as we get through this speculative phase of cryptocurrency’s development.

With cryptocurrency, we can put financial and monetary concepts into a crucible of fear, greed, and fraud to produce secure, robust, resilient financial systems that replace today’s patchwork of humans, governments, and rent-seeking entities.

Some may say we need the safety of government regulations and politicians who promise to do nice things for us.

The whole point of crypto is to escape the whims of governments, not ask them to do our bidding. Let governments provide for the common welfare. They don't need to control our money, too.

The safety we seek comes from the certainty of knowing our wealth is protected by strong, durable, self-sufficient networks forged by hacks, forks, competition, and regulatory attacks.

No government or politician can give us that.

“Safe” is a relative term

With legacy finance, safety is a myth.

Last year, US government bonds almost caused a banking crisis. In 2008, bad mortgages triggered a global financial meltdown. The Fed creates a new facility or program seemingly every other year to bail out some part of the US banking system and, by extension, the rest of the world’s.

I’m old enough to remember when the government made houses safe.

My parents called them “the best investment you can make.” The first step towards financial security. The pillar of the middle class. The housing market always goes up, right?

So you can understand why my wife and I put our life savings into a house in 2007. As a young couple eager to start a family, what better way to build our future and capture the American Dream?

Less than a year later, the housing market collapsed. We owed the bank $100,000 more than our house was worth.

With student loans, car payments, and no investments outside of maybe $5,000 in retirement accounts, that house made us insolvent. We couldn’t even afford to sell it.

Can you imagine your finances destroyed by the “safest, best investment” you could make? An asset protected by the courts, subsidized by the tax code, and promoted by the government?

Everything is risky

Crypto may not have courts, governments, or tax codes on its side, but it gives you a lot of upside for the risk you take.

Bitcoin is the best risk-adjusted investment you can make. No altcoin is worth its price today, but some will do so well that you have to take a stab at them.

Look at the alternatives.

Government bonds trade in opaque, manipulated markets. Their upside is capped, their yields are created out of thin air, and their rewards are dilutive.

Often, the government does not have enough money to pay the yield and must forcefully transfer wealth from its citizens to its creditors. Much of the demand comes from foreign speculators, sometimes from hostile regimes.

Stocks, then?

The Buffett Indicator, which measures the total market cap of US stocks relative to US GDP, hit an all-time peak this month, surpassing its previous high from November 2021.

P/E ratios, forward earnings, and market capitalization as a share of US GDP remain way above historical benchmarks.

Real estate?

Builders are completing new units at the fastest pace since 2007.

Operational costs and taxes have skyrocketed in the past two years. In many places, zoning laws now encourage developers to turn empty or underutilized commercial properties into mixed-use or residential developments, bringing more units to market.

Once the Fed starts cutting rates, people with low-interest mortgages will find it easier to move or downsize to newer or cheaper houses (because a new mortgage will cost less).

In other words, costs are higher, supply is growing, and you can expect more competition among landlords in the coming years.

Demand may fall off, too, if the US cuts immigration or too many people lose their jobs.

Eyes wide open

As a landlord with exposure to stocks and bonds, I can appreciate the risks of all types of “safe” investments.

Crypto may fall towards the extreme end of the spectrum, but with a reasonable approach, it will compensate you for the risks you take.

Even the shady stuff has an upside.

Several lending platforms imploded in 2022, but not before many people made money from the yield on their deposits.

Fortunately, we got out of Celsius and BlockFi before they collapsed (we left Voyager months before anybody sensed any problems with the lending platforms and for totally different reasons). I still have some legacy BTC on Ledn.

I know plenty of people who did well with meme coins, even though I don't trade them. Money is a social construct. Memes are fun. If you think you can make money with them, go for it.

I'm fine with DeFi. Sure, the smart contracts can fail and the protocols can get hacked. Try simple lending and depositing into liquidity pools with a portion of your assets. Free crypto (not risk-free crypto).

I have no problem with exotic financial engineering that creates high yields. As one of my subscribers said in an email, he made a lot of money off of UST. Why should I discourage you from trying the same thing with other platforms? You know the risks.

While LUNA was fraudulently pumped, the LUNA ecosystem had some innovative platforms and the Terra Station wallet had the best interface of its time.

You can lose money with all of these activities. (I lost 3% of my portfolio on LUNA.)

You can also make money. Good can come from bad.

At the end of the day, it's hard to quantify risk. Actuaries spend their entire lives trying to put objective numbers on risk/reward and still can't get it right. These are highly trained professionals with great intellect and years of training.

I'll bet some of those actuaries bought a house at the top of the US housing market, too.

Plan, don’t worry

Fortunately, we don't need to quantify risk. It's enough to acknowledge that it exists and plan accordingly.

How?

With my plan.

If you followed my plan, you're up 4% at worst, up 1,150% at best, and most likely up 150% with cash to spare. You sold some Bitcoin in March and some altcoins at the beginning of April.

Where you fall depends on when you started and whether you bought our most recent drop with new money or money you recycled from selling earlier this year.

This is what you’d have done with Bitcoin since 2023, after buying for most of 2022:

The plan doesn't apply to altcoins, but I discuss the altcoin market in my regular updates for premium subscribers.

As long as the “macro” cooperates . . .

The recessionistas say not to bother. Sahm rule’s about to trigger. Hard landing’s on its way. Your plans are useless.

I'm old enough to remember when they said the same thing about the yield curve inversion, rate hikes, and the Fed overtightening.

Long-time subscribers know I've prepared for a recession since the US economy reached full employment at the end of 2021.

The US always has a recession within five years of reaching full employment. Since 1970, recessions have come within three years.

We should get a US recession at the end of 2024, the end of 2026, or sometime between.

Unless our two consecutive quarters of negative growth in 2022 count as a recession. They used to, under the old definition of recession.

The Trump administration changed that definition to “a significant decline in economic activity spread across the economy and lasts more than a few months” with “no fixed rule about what measures [to include] or how they are weighted in our decisions.”

In other words, a recession is whatever the US government decides. Under this definition, we may never have a recession again.

For those who like data models, theories, and projections, look out for 2025.

The Beveridge Curve is on pace to hit its inflection point around March, the same time as the SPX will peak if it repeats the pattern we saw the last time it tapped the 100-year-old trendline shown below. 👀

And what about China?

It’s the world's second-largest economy and biggest trading partner. Persistent stimulus has kept its economy from collapsing. Will that translate into lasting growth and expansion?

I have met the retail investors, and they are us

Time will tell whether the macro matters as much as people think.

Certainly, it plays a role. It’s also unpredictable, and your government can change its impact with a wave of its magic wand.

Do you know what doesn't change and can’t be controlled with magic wands?

Human psychology. Namely, speculative bubbles.

We create them all the time. You can see this in the anatomy of a bubble chart.

If you, like me, believe crypto is a series of bubbles, large and small, over small and large time frames, repeated forever, then we can use this chart as a mental framework.

For a long time, I’ve wondered whether we’re in the middle of the “first sell-off” within a larger bubble cycle.

We have lots of circumstantial evidence to suggest this is valid. I’ve covered that evidence at length in my market updates, from quirks in unrealized profit metrics to accumulation patterns that seem to have only one explanation:

Large entities are buying, likely through brokers and funds.

Because these entities do not interface directly with the blockchain, DEXs, or exchanges, you can’t see their actions in the on-chain data or trading charts. You can only infer what’s going on.

You might think this means it’s too late for the little guy. “Institutions” have cornered the market.

No, not yet. At some point, certainly, but not today.

Get in while you can

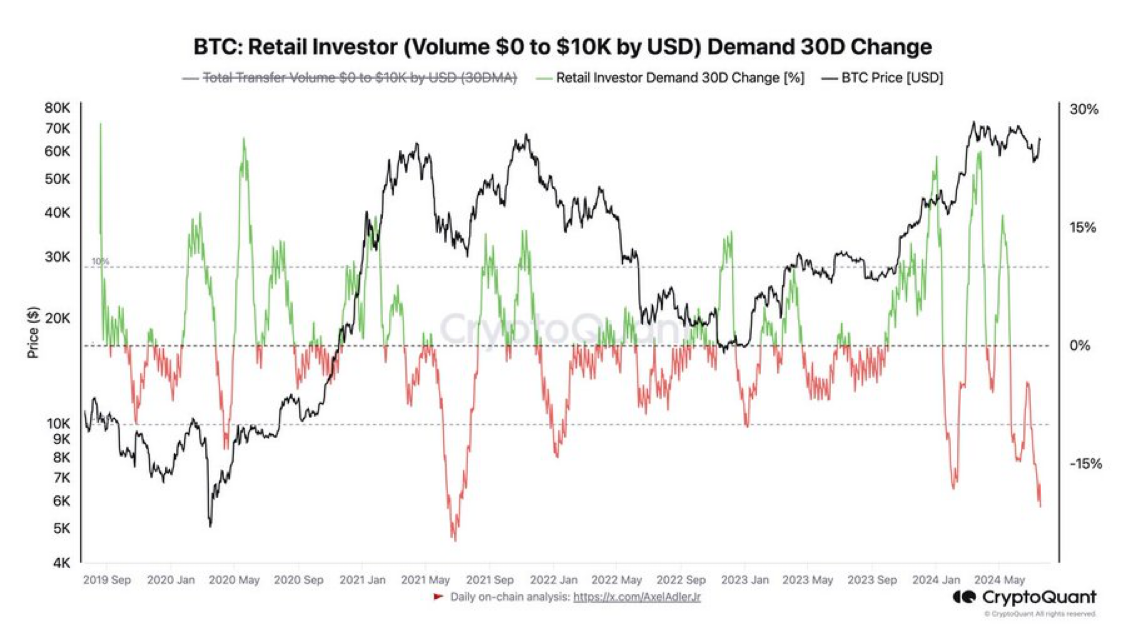

After bursting higher in February and March, retail investor volumes have dropped to their lowest since summer 2021. Premium subscribers saw this shift in real time, as it happened.

We can verify this in hindsight with the 30-day change in retail investor volume, as defined by Glassnode.

People either don’t have money or moved their money into something else.

Shame. Crypto remains the best market for retail investors like us.

In every other market, huge entities have access to the best data, analysts, technology, financial operators, and deals. You and I can’t compete.

With crypto, we can. We have on-chain data, technical analysis, and dashboards. Some of my favorites:

Many institutional investors don’t know these resources exist. Some think they’re hogwash. Others think their fund manager will do the research for them.

That’s our edge. We can see the data and the behaviors they represent. We can find the clues and put uncertainty to our advantage. This helps us navigate the ups and downs.

I bring these resources together for my market updates so you don’t need to spend thousands of dollars on data services. I distill the most important data into videos with written summaries, commentary, analysis, and charts.

For a sample of the email you’ll get, see my June 13, 2024 update.

Watch this snippet for a sample of the video content that goes with each email.

Others, though

What about your friends and family?

By the time they come into the market, the best opportunities will have passed. They will see prices going up, feel the urge to buy into the hype, and eventually sell into the fear that comes when the market rally inevitably falls.

They will look for charts and predictions that match their beliefs, regardless of whether those charts have any merit or connection to reality.

There's a reason people only subscribe to this newsletter after prices go up, not down.

The best opportunities come when nobody's looking and nobody cares.

People, on the other hand, come when there’s something to see and a reason to care.

Look out for them

When mainstream attention returns, Samantha Down the Street will ask you about crypto.

If you follow my plan, it’ll probably tell you not to buy. She won’t care. She’ll ask you, “Who the hell is this Bitmoji and why should anybody listen to him?”

She’ll want to buy and there’s nothing you’ll be able to do to stop her.

Protect her.

Tell her opportunities always exist. There’s never a bad time to buy Bitcoin. All altcoins are overpriced and none are safe. The best deals come after the market crashes (not dips). Moments of speculative frenzy come and go. Wait for them to pass before you start buying.

She won’t believe you, but at least you’ll plant the seed in her mind so when the market drops, she might have a healthy attitude about it.

What would happen if you told your friends and family about this newsletter, before the next big upswing? It's free.

They don’t even need to follow my plan! You can tell them to follow a simple, effective strategy that’s almost as good:

Buy Bitcoin blindly, on a fixed schedule, in a fixed amount, regardless of circumstances, forever. Never touch altcoins.

With that approach, they’ll beat most traders.

No problem with following “the herd,” either. They’ll come out ahead on their investment, too.

Consensus opinion told you to buy above $50,000 in 2021, sell at $40,000 in 2022, and buy again at $32,000 in 2023. With that approach, your $50,000 investment would grow to $75,000.

That’s a 50% return in three years! As good as any fund manager and hard to get from any other asset that’s so easy to buy, hold, and sell.

Not just that, it feels better. There’s a social consensus around your actions. You feel a sense of validation for your decisions.

The blind approach, dollar cost averaging, did better (ROI of 70% over that time). My plan did even better than that (ROI of 110% over that time, better if you sold when you read my alerts.)

Your impression is not reality

This may seem out of sync with what you see.

You’re not alone. Often, reality doesn’t match your expectations.

On the one hand, on-chain and technical data gave you the impression that we should’ve had a bigger drop-off than we've gotten since March. That's how extreme we got earlier this year, before the halving.

On the other hand, this year’s early mania gave you the impression that this market would go much higher, much more quickly than it has. That seemed like the consensus just a few months ago, now shattered.

Because nobody's getting what they expected, everybody's on edge.

If you’re new to the market, don’t worry. You still have tremendous opportunities, they just won’t necessarily come when you want in the way that you’re expecting.

Read my most recent special reports for a realistic view:

The hard part is figuring out how to apply this knowledge to your own life. For example, if you’re young, you have at least two good options:

Wait for Bitcoin’s price to go into the gray zone of my plan, at the risk of missing the next leg up. This can work because you’ll have many bear markets over the coming decades that will give you plenty of opportunities to buy at amazing prices in very low-risk, high-reward settings. You can save money for those bear markets and avoid a lot of volatility along the way.

Buy aggressively below the orange line in my plan, at the risk of buying too high. This can work because you have so many years to make up for bad timing with fresh cash. As a result, you don’t need to wait for very low-risk, high-reward settings.

Two opposite paths to the same destination. Both may deliver the same result over the next few years. You have plenty of other options beyond these two.

Pick an approach that helps you sleep better at night and stay allocated to the market.

Are you concerned about your cash position or your ability to make more of your government’s money?

Maybe you can cash out and come back in the next bear market. Or not.

Take a mental and emotional inventory. Would you feel worse if the market went up before you got your money in, or if the market went down and you had no money to take advantage of the downturn?

If you’re following my plan, you will always have money to take advantage of downturns, but if you start following the plan when Bitcoin’s price is outside of the buying zone, there’s a good chance the market will go up without you.

The plan assumes you already bought during the down times, getting more value as prices fell, so that when the market goes up again and everybody asks you why you’re not buying, you can tell them you already did.

That takes some courage. When the market starts zooming again, it will get harder to sit on cash and wait. You will need all your strength to resist the temptation to buy into the uptrend once it goes high enough that everybody else thinks it will keep going higher.

Fortunately, we're not there yet, but we might be soon. Make sure you'll know what to do when the time comes.

Relax and enjoy the ride!

Reply